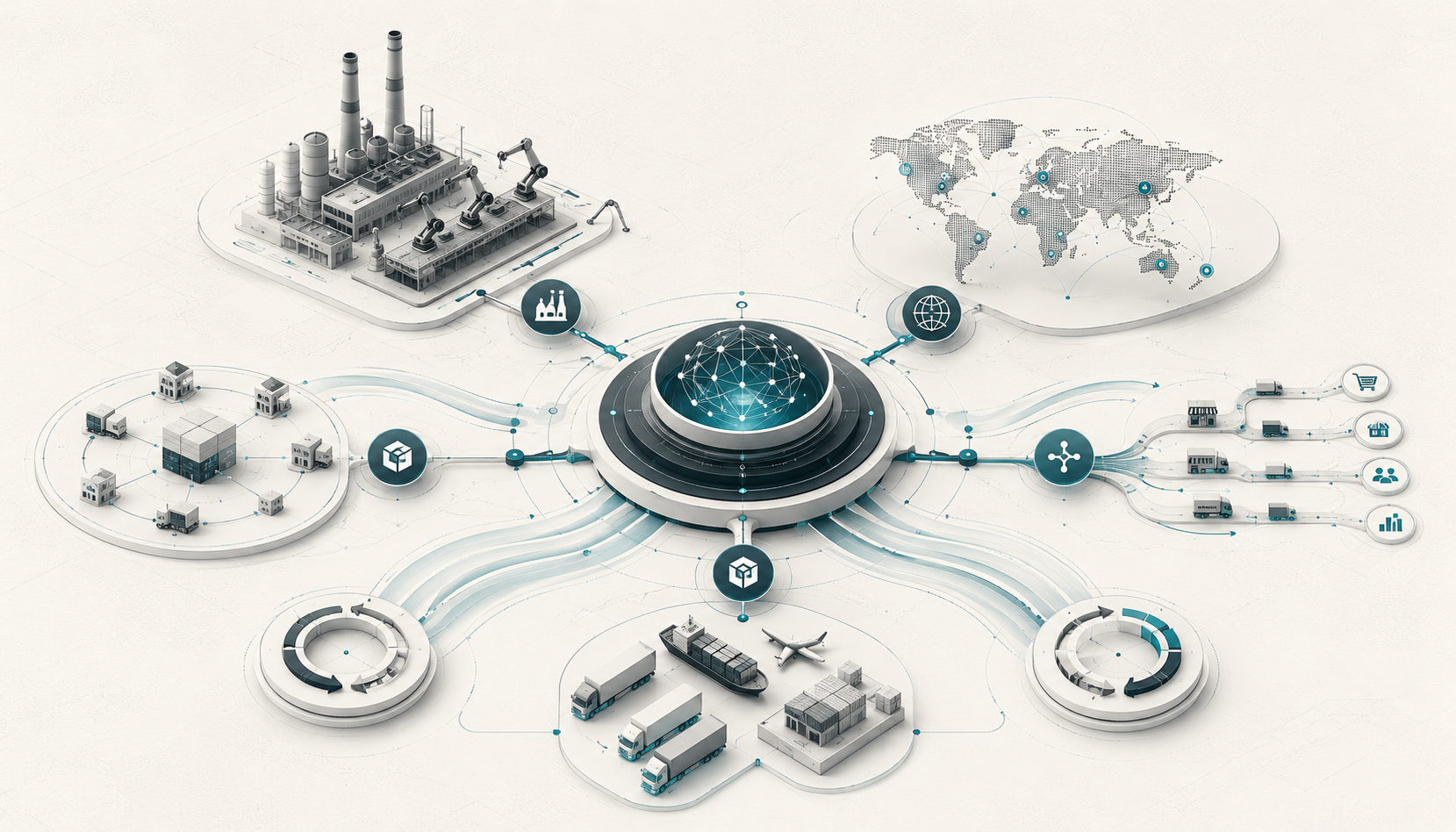

Global manufacturing is changing faster than it has in decades. Geopolitical tensions, nearshoring, and rapid growth in industrial automation are creating both opportunities and challenges for OEMs and suppliers worldwide. This article examines the main forces driving these changes, what is at stake, and the key steps companies need to take to stay competitive.

Three big changes are happening at the same time, reshaping global manufacturing. To respond well, it is important to understand how these changes connect.

For thirty years, global supply chains focused mainly on cutting costs. Companies sourced materials from cheaper regions, kept inventories low, and aimed to boost profits. Now, that approach has come to an end.

The COVID-19 pandemic revealed major risks of relying on a single supplier. The multi-year semiconductor shortage cost the auto industry an estimated $210 billion in lost sales. Russia’s invasion of Ukraine cut off energy and raw materials that European factories depended on. Escalating U.S.-China trade tensions, culminating in 125% tariffs on Chinese goods and a 10–15% baseline on most other imports following the April 2025 “Liberation Day” order, have pushed global companies to fundamentally rethink where they operate.

Because of this, companies are moving from 'just-in-time' to 'just-in-case' strategies. Resilience, backup plans, and spreading operations across regions are now driving real investment decisions, not just being discussed.

Reshoring has moved beyond politics and become a clear investment trend. In the United States, the CHIPS and Science Act ($52 billion), the Inflation Reduction Act ($369 billion for clean energy), and the Infrastructure Investment and Jobs Act have sparked a major surge in domestic manufacturing. Total announced U.S. private-sector manufacturing commitments have now surpassed $1.5 trillion, spanning semiconductors, advanced computing, pharmaceuticals, energy infrastructure, and critical materials.

In Europe, the European Chips Act aims to double the EU's share of global semiconductor production to 20% by 2030. Germany’s €17 billion investment in TSMC and Intel factories shows that reshoring is now a national priority, not just a test of subsidies.

Mexico has become the main hub for nearshoring in North America, with foreign investment in manufacturing FDI surging by more than 50% as companies sought proximity to U.S. markets and tariff advantages. New U.S.–Mexico trade tensions have since introduced uncertainty, prompting some firms to reassess sourcing strategies. Vietnam, India, and Poland are taking on similar roles in the Asia-Pacific and European supply chains.

Industrial automation has reached a turning point. Over the past ten years, the cost of using collaborative robots (cobots) has dropped by more than 70%, while productivity and flexibility have increased sharply. The International Federation of Robotics recorded 542,000 industrial robot installations in its most recent annual report, the second-highest total ever, with the global operational stock now exceeding 4.66 million units. Installations are projected to reach 575,000 in the next year and surpass 700,000 by the end of the decade, growing at approximately 10% annually.

The growth of AI-driven automation is just as important. Technologies such as machine vision, predictive maintenance, digital twins, and generative AI-assisted design are changing not only the factory floor but also the entire value chain, from procurement to quality management.

"The question is no longer whether to automate, but how fast you can deploy automation intelligently before your competitor does."

|

$46.7T |

Current global manufacturing output in 2025, reflecting sustained reshoring and greenfield investment momentum with the sector forecast to grow steadily through the end of the decade (Oxford Economics, 2025) |

|

542K |

Industrial robots installed globally in the most recent reporting year the second-highest annual total on record with the global operational stock now exceeding 4.66 million units and installations projected to surpass 700,000 before the end of the decade (IFR, World Robotics 2025) |

|

$1.5T+ |

Announced U.S. private-sector manufacturing commitments spanning semiconductors, advanced computing, pharmaceuticals, energy infrastructure, and critical materials up from $200B just two years ago (Reshoring Initiative / White House tracking, Feb 2026) |

|

+40% |

Surge in Mexico manufacturing FDI as nearshoring reshapes North American supply chains though recent U.S. Mexico tariff developments have introduced new uncertainty, prompting some firms to reassess long-term sourcing strategies |

|

70% |

Reduction in cobot deployment costs over the past decade, making automation economically viable for Tier-2 suppliers driving a cobot market now valued at $1.9 billion and projected to reach $4.9 billion by 2030 at a 20%+ CAGR |

The changes in manufacturing do not offer the same opportunities to everyone. Each tier faces different challenges, so leaders need to adjust their strategies to fit their specific situations.

For Original Equipment Manufacturers, the main challenge is wide-ranging and complex. They need to do more than simply move production. They must rethink how their supply networks are organized, considering factors such as proximity to customers, labor costs, access to skilled workers, and capital efficiency.

OEMs that move quickly can build strong relationships with suppliers in nearby markets, invest with them to develop skills, and set up new automated facilities that help keep costs down for years. Those who wait may find the best suppliers are already working with competitors and may end up paying more.

For CEOs and COOs at OEMs, it is important to view supply network redesign as a means to gain an advantage, not just to cut costs. The companies that will lead their industries in 2030 are already making these key investments.

Tier-1 suppliers face a tough set of challenges. They must meet OEM demands for nearshore capacity, invest in automation, and manage rising costs and talent shortages.

They often have less financial flexibility than their OEM partners while doing all this.

Some Tier-1 suppliers are turning these challenges into opportunities. By investing early in automation, digital tools, and flexible locations, they stand out as strategic partners rather than just vendors. OEMs are now more likely to offer long-term contracts, preferred status, and co-investment deals to Tier-1s that show they can adapt.

Tier-2 suppliers are often overlooked in the manufacturing reset. They work closest to the raw materials and components that determine if reshoring goals can be met, but they are usually the last to receive strategic investment or support.

The reality is clear: Many reshoring efforts will slow down, not because OEMs lack money or motivation, but because local and nearby Tier-2 suppliers lack the capacity, skills, or certifications to support large-scale production. This creates an urgent need for Tier-2 suppliers who are ready to invest in expanding capacity, improving quality systems, and getting ready for automation.

Private equity groups are bringing Tier-2 suppliers together, while government programs and OEM-led initiatives are helping these suppliers grow. These efforts are creating new funding opportunities for Tier-2 suppliers who act quickly and think strategically.

From our work with manufacturing leaders worldwide, we have seen that the companies benefiting most from these changes tend to follow a similar strategy. Their approach is guided by five main priorities.

Before deciding on reshoring or nearshoring investments, leaders need a clear, detailed understanding of their supply network’s vulnerabilities. This involves mapping single-source dependencies, estimating the costs of possible supply disruptions, and testing the network under different geopolitical and tariff situations.

Companies that have made costly reshoring mistakes often share one problem: they picked locations before fully understanding their real weaknesses and where most of their value was concentrated. A thorough network diagnostic is essential and forms the basis for all future decisions.

Companies should avoid making automation investments just to address short-term labor shortages. Leading organizations are creating structured, multi-year automation plans that prioritize investments based on ROI, strategic importance, and implementation complexity.

It is important to connect the automation plan with the workforce strategy. Successful companies are not just replacing workers; they are retraining and upskilling employees and moving them into higher-value roles. This approach is both ethical and necessary for operations. Today, the main challenge in automation is not money or technology, but finding the engineering and integration talent needed to make it work well.

The opportunity to secure government incentives such as tax credits, grants, co-investment programs, and subsidized financing will not last forever. Programs such as the IRA's Advanced Manufacturing Production Credit, the CHIPS Act's FABS tax credit, and the EU's Important Projects of Common European Interest (IPCEI) framework offer significant capital subsidies, but they will not be available indefinitely.

Manufacturers without dedicated teams for government affairs and incentive capture are missing out on available capital. This is not just a compliance task; it is a strategic financing role that should be a board priority.

OEMs and Tier-1s that want resilient supply chains by 2030 are already investing in their suppliers. They share technical expertise, offer financing support, and sometimes take equity stakes in key Tier-2 and Tier-3 suppliers.

Focusing on supplier development turns procurement from just cutting costs into building strategic capabilities. It also creates switching costs and strong partner relationships that are hard for competitors to copy.

Supply chain visibility, meaning the ability to track inventory, production status, and disruption signals across different levels in real time, is now a basic requirement rather than just a competitive edge. The pandemic highlighted this need, and ongoing geopolitical disruptions have only increased the demand for real-time visibility.

Besides visibility, top manufacturers are now using AI-driven demand sensing, digital twin simulations to optimize their networks, and automated procurement systems that can quickly adjust sourcing when disruptions occur. These tools are not science fiction; leading companies are already using them, and the gap between industry leaders and others is growing quickly.

The strategic value of acting now, rather than waiting for greater certainty or studying the situation longer, is unusually high. Three factors are making the decision window much shorter than most manufacturing executives have seen before.

First, incentive capital is finite and competitive. Government programs are oversubscribed in many sectors, with manufacturing site selection processes in the U.S. and Europe increasingly resembling auctions for limited incentive pools. The firms that complete their strategic assessment quickly and move to implementation have meaningful capital advantages over those that arrive late.

Second, skilled trades and engineering talent are already in short supply. Updated projections put the U.S. manufacturing talent gap at up to 1.9 million unfilled roles by the early part of the next decade, with hundreds of thousands of positions already vacant today (Deloitte/Manufacturing Institute). The firms that build training pipelines, establish community college partnerships, and develop automation integration expertise now will have structural talent advantages that cannot be quickly replicated.

Third, supplier commitments are being locked up. As reshoring investment accelerates, the best-positioned nearshore and domestic suppliers are receiving long-term offtake commitments from early movers. OEMs and Tier-1s that delay risk finding that preferred supplier capacity has been committed to competitors.

Across the sectors most affected by the manufacturing reset, automotive, aerospace and defence, medical devices, industrial equipment, consumer electronics, and clean energy, a clear pattern is emerging in how the highest-performing firms are operating.

They have made supply chain strategy a top priority for CEOs and boards, not just a functional topic. They are making investment decisions much faster than they would have three years ago, not because they have lost financial discipline, but because they know that waiting now is riskier than acting. They are also building organizations that can learn and adapt faster than the environment is changing.

At its core, the manufacturing reset is a test of leadership. Deciding where to nearshore, what to automate, and which incentive programs to pursue are important, but these are problems that can be solved. The bigger challenge is building the conviction, speed, and change-management skills needed to act as quickly as this moment demands.

The convergence of reshoring, robotics, and resilience is not just a short-term market trend. It is a major shift in global manufacturing that will unfold over the next decade. The competitive positions set in the next 24 to 36 months will likely last for a long time.

For OEMs, Tier-1, and Tier-2 suppliers, the question is not whether to take part in this reset, but how to do so with a clear strategy, efficient use of capital, and the urgency that this moment requires.

The companies that will look back on this decade as the time they built their competitive advantage are those moving now with focus, confidence, and the right partners to handle the complexity.

The global manufacturing reset is not something in the future. It is already happening, and the gap between companies taking action and those still analyzing is growing every quarter.

At Velox, we work with OEMs, Tier-1, and Tier-2 manufacturers who are facing these key decisions: where to reshore, how to automate smartly, which incentives to pursue, and how to build supply chains that are truly resilient, not just less fragile than before.

What we have seen in our work matches what the data shows: the manufacturers who will shape the next decade are not waiting for certainty. They are building networks, securing supplier relationships, and rolling out automation plans now, while incentive capital is still available and the best domestic and nearshore partners still have capacity.

Our work spans the full strategic journey:

The companies we work with are not making these decisions alone. They are combining careful operations with strategic urgency, because in this environment, a six-month delay often leads to years of competitive disadvantage.

If your organization is assessing its position in the manufacturing reset, we'd welcome the opportunity to discuss it.

What is reshoring?

Reshoring is bringing manufacturing operations back to your home country after years of offshoring. It's accelerating in 2025–2026, driven by tariffs, supply chain risk, and $1.5T+ in U.S. government manufacturing incentives.

What's the difference between reshoring and nearshoring?

Reshoring = manufacturing back home. Nearshoring = manufacturing in a closer country (e.g., Mexico instead of China). Both reduce risk, cut lead times, and respond to tariff pressure.

Why is industrial automation growing so fast?

Cobot costs have fallen 70% in a decade, making automation viable even for Tier-2 suppliers. Global robot installations hit 542,000 units in 2024 and are projected to surpass 700,000 by 2030.

What U.S. incentives are available for manufacturers?

Key programs include the CHIPS Act ($52B), the Inflation Reduction Act ($369B in clean energy manufacturing), and the FABS tax credit. These are competitive and time-limited; early movers win more capital.

What is a 'just-in-case' supply chain strategy?

It's the shift away from lean, single-source "just-in-time" supply chains toward resilient, diversified ones with backup suppliers and safety stock, a direct response to COVID-era disruptions.

What's the risk of waiting to act?

Incentive pools are being claimed. Supplier capacity is being locked up. The U.S. faces a 1.9M manufacturing talent gap by the early 2030s. A 6-month delay often means years of competitive disadvantage.

Which industries need to move fastest?

Automotive, aerospace & defense, MedTech & pharma, clean energy, and semiconductors face the most immediate pressure from reshoring mandates, domestic content rules, and supply chain restructuring.

How can Tier-2 suppliers capitalize on the manufacturing reset?

By investing now in capacity, automation, and quality certifications. OEMs are actively seeking reliable domestic partners, Tier-2s that move first are landing long-term contracts and co-investment deals.